US carriers are already filing AI exclusions across D&O, E&O, and general liability. The London market is still writing. That gap is the window. The view out that window is uncertain.

Your policy renewed. The summary looked familiar. Nobody mentioned AI. But across the Atlantic, carriers are filing exclusions that remove AI cover entirely from directors and officers, errors and omissions, and general liability policies. The London market has not followed yet. It is still surveying and researching. That does not mean the language is not coming. It means you have time to read it before it arrives.

The US Market Has Already Moved

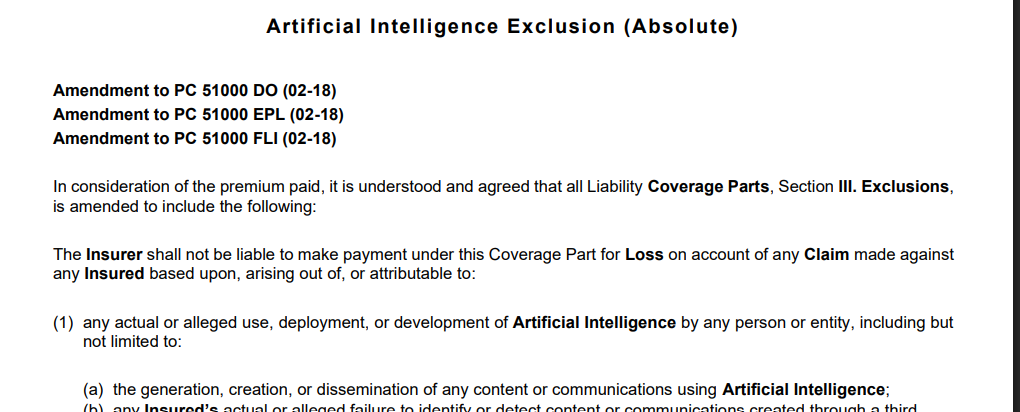

Berkley Insurance introduced what the market calls an “absolute” AI exclusion applied across D&O, E&O, and Fiduciary Liability. It excludes any claim “based upon, arising out of, or attributable to” the use, deployment, or development of artificial intelligence by any person or entity. Six enumerated categories cover AI generated content, failure to detect AI produced materials, inadequate AI governance, chatbot representations, and regulatory actions related to AI oversight. The definition is sweeping: any machine based system that infers from input how to generate outputs such as predictions, content, recommendations, or decisions. This is not a narrow carve out. It is a blanket removal of cover.

Hamilton Insurance Group took a different approach. Its generative AI exclusion for professional liability names specific platforms ChatGPT, Bard, Midjourney, DALL·E and excludes any claim involving actual or alleged use of generative AI by the insured.

Verisk, whose ISO forms underpin approximately 82 per cent of global property and casualty policy templates, made new general liability exclusion endorsements available from January 2026. These allow carriers to exclude bodily injury, property damage, and personal or advertising injury arising from generative AI. Verisk’s own personnel predict rapid adoption. When these become standard, the exclusion is no longer carrier-specific. It is market-wide.

Why does this matter to UK businesses? Carriers do not respect country boundaries. Many insurers writing UK technology risks operate across both markets. When claims become transnational and AI claims will the language follows. A UK technology company with US clients, US data, or US-incorporated AI tools in its product is already exposed to these wordings.

The London Market Is Still in the Research Phase. That Is the Window.

The Lloyd’s Market Association surveyed 144 managing agents in mid-2025, 94 per cent of them underwriters, to assess AI loss scenarios across professional indemnity, cyber, product recall, and accident and health. Professional indemnity was rated the highest potential impact. But the LMA explicitly states its observations do not relate to specific losses, wordings, or exclusions. The market is gathering intelligence. It has not yet acted on it.

https://lmalloyds.com/lma-survey-maps-underwriters-views-of-ai-loss-scenarios-across-key-lines

The LMA also reviewed its suite of model cyber clauses against AI risk. It recognises AI as a subset of software and therefore falling within the definition of “Computer System” used across Lloyd’s model cyber wordings. Depending on which clause your policy uses, AI may be affirmed, sub-limited, or excluded. Cyber clauses remain mandatory for nearly all classes written on Lloyd’s paper. This means the current AI coverage position for most London market policies is determined by a cyber clause most buyers have never checked.

Kennedys has warned directly that silent AI presents the same risk as silent cyber, exposures sitting unnoticed in existing wordings until a claim forces the question. Lockton’s head of cyber and technology insurance stated publicly this month that a mandate to clarify whether AI should be covered or not is coming, paralleling the Lloyd’s directive that forced clarity on silent cyber from 2020. And Airmic, the UK risk management body, confirms that AI-specific exclusions are not currently market standard but warns that implementation is entirely possible as the risk profile develops.

The gap between the US and UK market is not safety. It is timing. The US has moved because US litigation is further advanced. The London market is gathering the intelligence that will inform the same move. For the UK founder, this gap is the window to act.

The Affirmative Market Is Already Writing at Lloyd’s

Armilla, the first managing general agent exclusively focused on AI insurance, launched affirmative AI Liability Insurance at Lloyd’s in April 2025, underwritten by Chaucer Group and backed by Axis Capital and Swiss Re. The policy covers AI underperformance, hallucinations, model errors, regulatory violations, and data leakage. Purpose-built for AI risk, not a legacy form with an endorsement bolted on.

Google partnered with Beazley, Chubb, and Munich Re to create tailored affirmative AI coverage for Google Cloud customers. Munich Re, the reinsurer that ranks AI as the number one cyber security challenge and models accumulation potential at $20–46 billion, is writing affirmative AI cover. The market considers this an insurable risk. It just requires purpose-built wordings.

Three things to do before your next renewal. First, ask your broker which LMA cyber clause is attached to your policy and whether it affirms, sub-limits, or excludes AI exposure. Second, ask whether any AI related endorsement language, from any jurisdiction, has appeared in your programme. Third, ask about affirmative AI cover. It exists at Lloyd’s. It is being written now. The companies that access it before the mandate arrives get the best terms.

The Language Is Coming. Read It Before It Arrives.

The US market has filed the exclusions. The London market is drafting the questions. The founders who have read the language before it arrives in their wording are the ones with cover that responds when it matters.